SST Info

📌 Info updated as of 14 July 2025

Frequently Asked Questions (FAQ): SST 2025 – Higher Education for Non-Malaysian Citizens

-

1. What is SST?

SST stands for Sales and Service Tax, a tax imposed by the Malaysian government on certain goods and services.As gazetted by the Malaysian government on 9 June 2025, service tax at a rate of 6% will be applied to higher education services, effective 1 July 2025. This is part of a broader taxation policy adjustment under SST 2.0. This service tax is charged by and payable to the Government of Malaysia.

2. Who is impacted by this new SST legislation in Monash University Malaysia?

This service tax applies to non-Malaysian citizens to whom Monash University Malaysia provides education services.Malaysian citizens holding an identity card issued by the National Registration Department of Malaysia, and holders of a valid Disable Persons (OKU) card issued under the Persons with Disabilities Act 2008 [Act 685] are exempted from this charge.

-

1. Which services are subject to service tax?

- Tuition fees

- Application fee

- Registration fee

- General amenities fee

- Academic transcript & Courier charges

- Student letter request & Courier charges

- Instalment admin fee

- Late discontinuation charge

- All other charges related to education services

2. Which fees are not subject to service tax?

- Student Pass & Insurance

- Study trips abroad

The above is inclusive of, but not restricted to, any items not mentioned above depending on update from Malaysian authorities.

Eg (a) - Tuition fee billing with General Amenities & Registration feeStudent A has enrolled into Course A and he is billed tuition fee of RM30,000 + 6% service tax of RM1,800 = RM31,800 per semester. He is also billed General amenities fee and registration fee with 6% service tax. The total payable by student is:

Amount Service Tax Total General amenities fee 100.00 6.00 106.00 Registration fee 200.00 12.00 212.00 Tuition fee - Course A 30,000.00 1,800.00 31,800.00 Total to be paid by Student 30,300.00 1,818.00 32,118.00

3. I currently have a tuition fee waiver from Monash University Malaysia. Am I charged service tax on the full tuition fee or on the net tuition fee after deducting the waiver?Service tax will be charged on the full tuition fee amount, regardless if the student has a tuition fee waiver or not.

Eg (b) Tuition fee billing with partial tuition fee waiver

Student A has enrolled into Course A and he is billed tuition fee of RM30,000 + 6% service tax of RM1,800 = RM31,800 per semester. He is also billed General amenities fee and registration fee with 6% service tax. At the same time, Student A has a High Achiever Award tuition fee waiver of RM5,000. The total payable by student is:

Amount Service tax Total General amenities fee 100.00 6.00 106.00 Registration fee 200.00 12.00 212.00 Tuition fee - Course A 30,000.00 1,800.00 31,800.00 High Achiever Award waiver (5,000.00) 0.00 (5,000.00) Total to be paid by Student 25,300.00 1,818.00 27,118.00 This applies to students with varying types of tuition fee waiver for all courses.

Eg (c) Tuition fee billing with full tuition fee waiver

Student B is a Higher Degree of Research (HDR) student with a full tuition fee waiver. He has enrolled into Course A and he is billed tuition fee of RM30,000 + 6% service tax of RM1,800 = RM31,800. He is also billed general amenities fee and registration fee with 6% service tax. At the same time, Student B is offered a full tuition fee waiver. The total payable by student is:

Amount Service tax Total General amenities fee 100.00 6.00 106.00 Registration fee 200.00 12.00 212.00 Tuition fee - Course A 30,000.00 1,800.00 31,800.00 High Achiever Award waiver (30,000.00) 0.00 (30,000.00) Total to be paid by Student 300.00 1,818.00 2,118.00 This applies to students with full tuition fee waiver for all courses.

4. I am a sponsored student, and my tuition fees are paid in full by my sponsor. Do I need to pay service tax?Your tuition fee and service tax will be billed to the sponsor who is liable for the payment of the same.

5. What if I add or drop unit(s)?If you add an unit, you will be billed tuition fee including service tax for the unit. Similarly, if you drop a unit, your fee statement will also be adjusted where the tuition fee and service tax for the dropped unit will be deducted from your balance.

Eg (d) - Add/Drop units

Date Amount Service

TaxTotal Tuition fee - Unit A 15.07.2025 7,500.00 450.00 7,950.00 Tuition fee - Unit B 15.07.2025 7,500.00 450.00 7,950.00 Tuition fee - Unit C 15.07.2025 7,500.00 450.00 7,950.00 Adjustment for tuition

fee - dropped Unit A01.08.2025 (7,500.00) (450.00) (7,950.00) Adjustment for tuition

fee - added Unit D12.08.2025 7,950.00 450.00 7,950.00 Total to be paid by

Student22,500.00 1,350.00 23,850.00 -

1. I have not received my Fee statement. How do I know how much to pay?

Billing for Semester 2, 2025 will be issued in July 2025 as we are upgrading our system for SST compliance. The Fee calculator with service tax function will be available on our website by July 2025 so that you can calculate the total fee that you need to pay. The payment due date for Semester 2, 2025 is 1 August 2025. You are advised to make payment based on your enrolled units as calculated in the Fee calculator prior to receiving your Fee statement.2. Will I be charged service tax if I have paid my fees before the effective date?

To date, the guidelines from Malaysian authorities have stated that payment received before 1 July 2025 is not subject to service tax. Service tax will be chargeable from 1 July 2025.Should there be any further update from Government authorities, we will provide updates in this FAQ

3. Can I get a refund of service tax if I withdraw?

Service tax is a government tax that Monash University Malaysia collects from the students on behalf of the Malaysian authorities. Refunds will follow the University’s standard withdrawal and refund policy, and service tax will be addressed accordingly in line with tax guidelines.HOW TO READ MY FEE STATEMENT - Info updated as of 14 July 2025

Below are some fee statement samples of an international student (non-citizen) and are for illustration purposes only. Students are highly encouraged to read the below guide for immediate information.

For information, amounts in brackets denote advance payment, payment and/or excess balance.

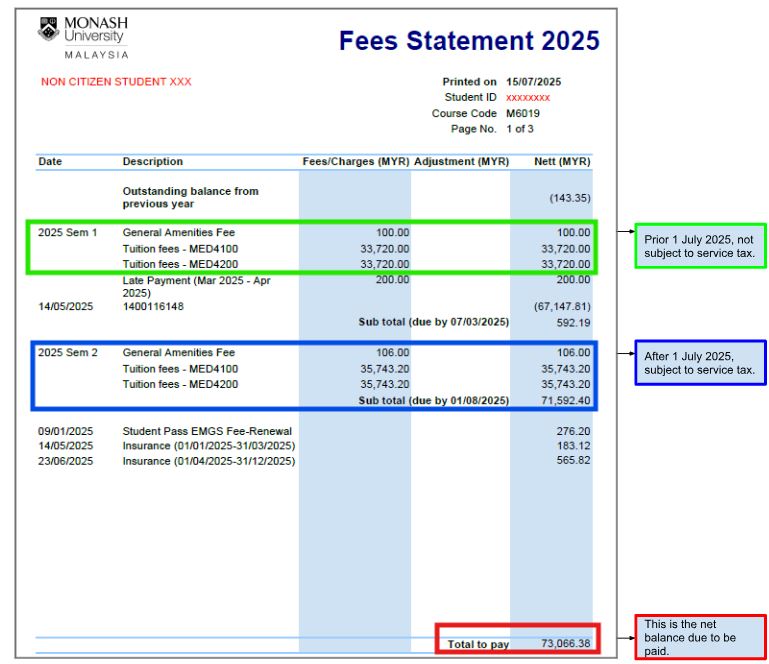

Eg (a) Tuition fee billing with service tax

- Before 1 July 2025, tuition fee and education charges are not subject to service tax. In the green box (Semester 1,2025) you will note that the fees do not include service tax.

- Effective 1 July 2025, tuition fees and educational charges are subject to service tax at the rate of 6%. In the blue box, you will see the tuition fee per subject unit for Semester 2, 2025 includes service tax (RM33,720.00 + 6% being RM2,023.20 = RM35,743.20). This applies to general amenities fees too.

- You can refer to the red box “Total to pay” for the net balance.

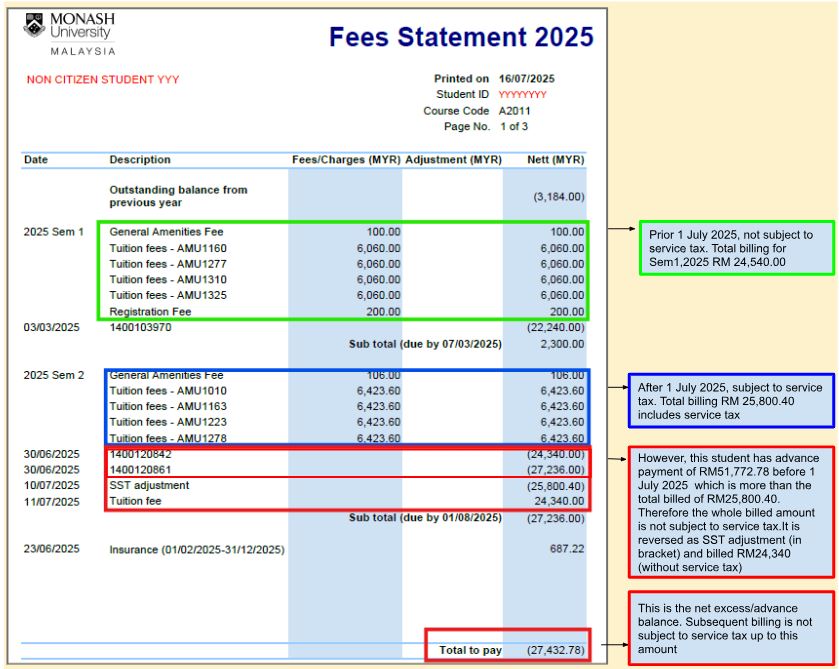

Eg (b) Tuition fee billing with service tax, where advance payment is more than billing

- Before 1 July 2025, tuition fee and education charges are not subject to service tax (green box).

- Effective 1 July 2025, tuition fees and educational charges are subject to service tax at the rate of 6%. In the blue box, you will see that the tuition fee per subject unit for Semester 2, 2025 includes the service tax (RM 6,060 + 6% being RM 363.60 = RM 6,423.60). This applies to general amenities fees too.

- Payment received before 1 July 2025 is not subject to service tax.

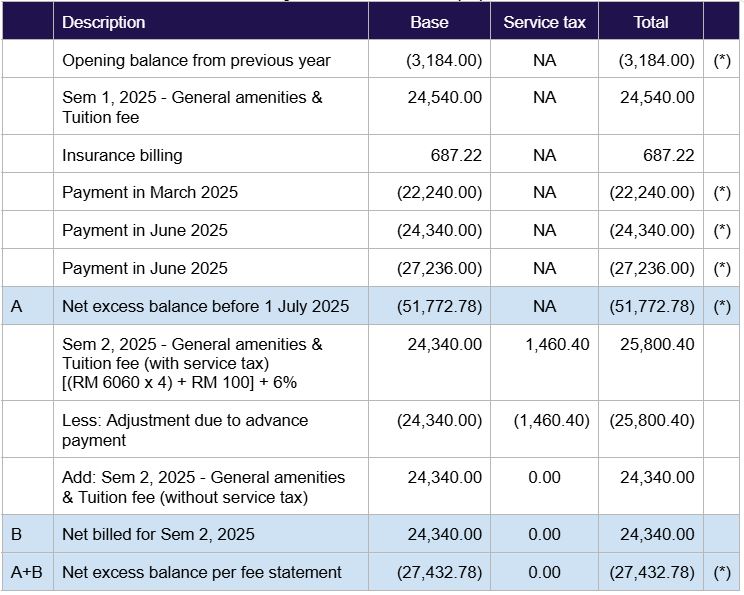

In this example, the student has an excess/advance balance of RM 51,772.78, before 1 July 2025 - refer to (A) below.

(*) amounts in brackets denote advance payment and/or payment.- In the meantime, tuition fee + general amenities fee including service tax for Sem2,2025 is RM 25,800.40 (blue box). As the advance payment of RM 51,772.78 is more than the charges for Sem 2,2025, this means the charges for Sem 2,2025 of RM 25,800.40 is not subject to service tax.

- In the red box, you will see that we have made adjustment as follows:

- Reverse the charge of RM 25,800.40 that included service tax; and

- Bill the tuition fee and general amenities of RM 24,340.00 that is not subject to service tax (red box) because this was paid in advance.

- After the above, there remains a net excess payment of RM 27,432.78. Subsequent billing is not subject to service tax up to this amount.

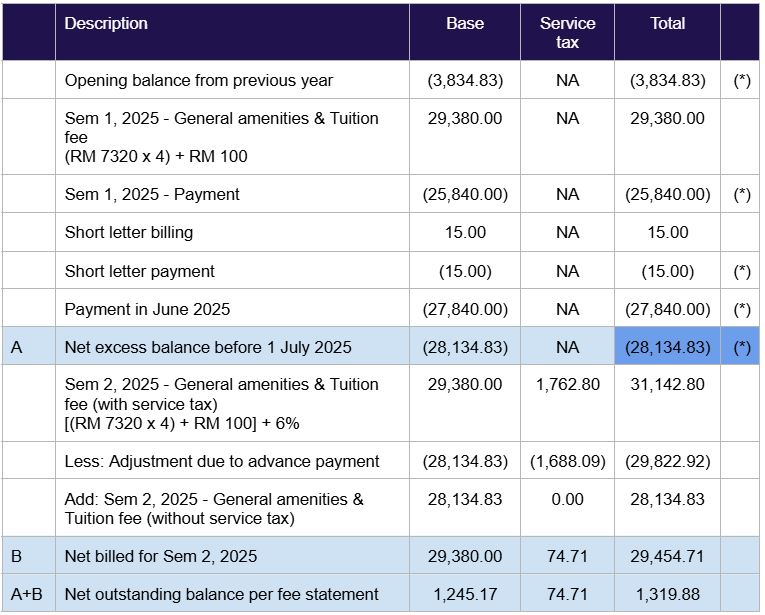

Eg (c) Tuition fee billing with service tax, where advance payment is less than billing

- Before 1 July 2025, tuition fee and education charges are not subject to service tax (green box).

- Effective 1 July 2025, tuition fees and educational charges are subject to service tax at the rate of 6%. In the blue box, you will see that the tuition fee per subject unit for Semester 2, 2025 includes the service tax (RM 7,320 + 6% being RM 439.20 = RM 7,759.20). This applies to general amenities fees too.

- Payment received before 1 July 2025 is not subject to service tax.

In this example, the student has an excess/advance balance of RM 28,134.83, before 1 July 2025 - refer to (A) in table.

(*) amounts in brackets denote advance payment and/or payment.- As the advance payment of RM 28,134.83 is less than the charges for Sem 2,2025 of RM31,142.80, this means only RM 28,134.83 is not subject to service tax.

- In the red box, you will see that we have made adjustment as follows:

- Reverse the charge of RM 29,822.92 that included service tax; and

- Bill the tuition fee RM 28,134.83 that is not subject to service tax (red box) because this was paid in advance before 1 July 2025.

- After the above, there remains an outstanding balance of RM 1,319.88 due to the University that needs to be paid.

Any subjects add/drop will be reflected in your Fee statements after intake week. You can add or deduct the amount when you make payment by using the fee calculator.

All tuition fee waivers and discounts will only be billed and reflected in your Fee statements after census date, 31 August 2025. You can deduct the amount when you make payment.

-

1. Will service tax affect new and continuing students?

Yes. All new and continuing non-Malaysian students will be subject to service tax on eligible fees charged on or after the effective date. -

1. Is this policy in line with Malaysian law?

Yes. The implementation of SST on private education services for non-Malaysian students is mandated under the Sales Tax Act 2018 and Service Tax Act 2018, with enforcement by the Royal Malaysian Customs Department.2. Where can I learn more about SST from the government?

You may visit the Royal Malaysian Customs Department website at https://www.customs.gov.my for official updates and public guidance.